INTRODUCTION

This essay is being written in March, 2018. Its purpose is to show you that there is a colossal financial shipwreck coming and help you get your life raft ready. To do so I will first sail you through the voyage of our global currency system from 1900 to the present. Then I will tell the tale of the near fatal sinking of the global financial system in 1998. We nearly hit an iceberg back then but it’s an episode very few of us are aware of. I will then recount the events of the great 2008 global financial storm, an episode all of us are aware of, and which brought us to within a day or two of sinking every bank on the planet. We actually scraped an iceberg in 2008, but it didn’t quite sink us. Then I will describe the current state of the voyage, arguing that we are about to witness events that will make 1998 and 2008 look like curtain-raisers to the main show. I see a huge financial iceberg dead ahead. Finally I will show you how you can grab hold of a financial lifejacket, preserve your savings and stay afloat when we do hit the inevitable.

This essay will focus on events in the USA, as that is the world’s undisputed financial powerhouse, centre of banking, monetary regulation, and generator of 23% of global GDP. When the USA sneezes, we all catch a cold. From time to time I will reference events in my home country, Australia, for the benefit of local readers. I trust what I have written can be of some assistance as you navigate your own significant icebergs, reefs and shoals over the next few years.

THE EVOLUTION OF OUR MONETARY SYSTEM

In the USA of 1899, you could take an ounce of gold into a bank and exchange it for a paper receipt with $20 written on it. That’s all a paper dollar was, a receipt. If you gave that paper receipt to a shopkeeper, they could take it to a bank and exchange it for an ounce of gold. I know this because I own an American ounce of gold made in 1899 and it has $20 stamped on it. There was no central bank at that time because the gold standard was all the discipline needed to run the US banking system. Today, in 2018, that same $20 dollars is worth 1/67 of an ounce of gold. The US dollar Is interchangeable with nothing and is devaluing every day of every year. What happened?

In 118 years the Western world’s currency system has moved from a classical gold/silver standard, to a quasi-gold standard after World War One, to banning the ownership of gold in the Great Depression, to a US global reserve currency backed by gold at $35 an ounce after World War II, to a totally fiat monetary system from 1971 until the present. Fiat means money backed by nothing, made legal by government decree, or else! The Bretton Woods agreement of 1944 marks the beginning of the first half of the modern global financial system, one based around the US dollar. The closing of the “gold window” by President Nixon in 1971 marked the beginning of the second half of the modern currency system.

President Nixon’s decree was a watershed in world history. Within a short time of that decision, every country in the world also had to go off the gold standard. Thousands of years of free market money and monetary wisdom was abandoned in favour of essentially socialist currency, money arbitrarily decreed by manipulative central governments and enforced by law. This had been tired in several places previously, but never on a global scale. We are seven and a half billion rats inside the world’s largest ever financial experiment, and most of us do not know we are in it, how we got there, or how it will end.

Religion is that which is believed to be ultimate truth by a civilisation, it decides all else in a culture, and that includes all things financial. Therefore this radical experiment in fiat currency mirrors the spiritual evolution of Western culture from a foundation of Judeo-Christian values, with an emphasis on sound money (Leviticus 19:36), to the atheism and fiat currencies of today. The eighth (theft), ninth (deception) and tenth (coveting) commandments are currently being violated by today’s fiat currency system. All of history is a battle between the sovereignty of our creator and the rebellion of humanity. This is why modern standards of art, behaviour, ethics, sexuality, entertainment, education, law, finance and commerce are decided according to the prevailing belief in the independence and sovereignty of humanity. Spiritual decline is followed by moral decline, financial decline, belief in the sovereignty of the state and an explosion of debt-fuelled lifestyles. They are all connected. A fiat money supply that is created from nothing is an attempt to sidestep the curse of scarcity handed down to Adam in the garden (Genesis 3:17-19). In the final section of this essay I will explain the Biblical principles of finance that are the solution to our current problem, in more detail.

Divine wisdom and truth will not be mocked. The fiat tower of Babel that we have created over the last three generations is in reality a tower built on sand. The current global financial system is only some 75 years old, a blink of the eye compared to world history. Like a 75 year old ship, it is groaning under the weight of its own rusting infrastructure and will soon collapse. Our system began when the Bretton Woods agreement transferred reserve currency status from the British pound to the American dollar. America owned half the world’s gold by the end of World War II, so the US dollar was king, and was made convertible into gold at $US 35 an ounce so the rest of the world’s governments would trust it in international trade. However, it was only convertible for foreign governments, not individuals. All other governments then fixed their exchange rates to the dollar. The system worked well until America started printing too many dollars to finance the Vietnam War and a parallel domestic war on poverty.

By 1971 America had abused its reserve currency status so much because of these two financial burdens that there was a run on its dollar. France led a consortium of countries demanding gold for their increasing pile of paper US dollars. Plane loads of gold left the USA permanently between 1970 and 1971. Its gold stocks halved and were going to zero. The US dollar was about to collapse. So, on the 15th of August 1971 Richard Nixon closed the gold window, releasing the world from the discipline of a gold standard once and for all. The currencies of the world were now adrift in an ocean of human ill-discipline and greed, free to sink or swim according to the strength of character of the politicians behind them.

The era of global fiat currencies had begun. One where money had become merely currency and not backed by intrinsically valuable commodities. It was all about faith in governments. Temptation proved irresistible and inexperienced governments the world over began to flirt with inflationary policies. Gold, always the barometer of government stupidity, peaked at $US850 an ounce in January of 1980, a 25 fold increase in just nine years. Actually gold had not moved in price, all the worlds’ currencies had sunk rapidly. Interest rates also went through the roof. People suffered terribly. As a teenager I saw and lived through the results of annual double digit inflation all around me. It was a time of such crisis that many Europeans refused to accept US dollars from American tourists. To preserve its failing reserve currency status after leaving the gold standard, America persuaded and/or forced the world to trade all oil in US dollars. Now the dollar was backed by oil. Now everyone needed their currency again. The petro-dollar was born, backed and imposed by the might of the American military to this day.

Free from the discipline of the last vestiges of the gold standard, banking practices evolved rapidly in the 1970’s and 80’s, creating marvellous new financial toys with which to speculate on global markets. One new toy was derivatives, which would in turn nearly destroy the worlds banking systems twice in 1998 and 2008. The Chicago-based monetarist school of economics told governments they needed an ever-expanding money supply to facilitate economic growth. This extra currency supply would come from new bank loans. So from the Seventies until now now new money would always come from new debt via fractional reserve banking. Your money was now simply someone else’s debt. Undisciplined fractional reserve banking meant that money was raining from the skies, inflation was in double digits and industrial unrest was normal.

The Keynesian school of economics told governments it was their job to modify the business cycle, to meddle with free markets, to run deficits during recessions. The seven to ten year boom-bust economic cycle was born. The trouble was, governments never paid off their debts when the good times returned. Today their debts reach the moon! Then central banks became the master puppeteers of the system, manipulating interest rates to control capitalism and issuing currency from nothing on government demand. All these agents of control, influence and manipulation were needed to keep the good ship Fiat heading in the right direction. But the ship was taking on an ever-increasing ballast of debt to do so.

Private debt became a new way of life for many expanding baby boomer families who no longer had personal memories of the Great Depression. Banks also loosened practices they had inherited from the great depression. It made perfect sense to borrow today and pay a loan off with cheaper, inflated currency in the future. Governments did the same. Of course with all this new money, home prices and stock markets took off in a way never seen before. The price of consumer goods also took off, impoverishing savers and enriching speculators.

This brief summary of the 20th Century Western financial system is a very simple description of the core of the current global financial architecture. It is the only system nearly all of us have ever known. Anyone under seventy knows nothing else. However, when you look at it objectively, there is nothing inherently right or righteous about our current financial superstructure. In fact it is in many ways a dreadfully dysfunctional system. Consider the following:

1. It relies on ever-expanding debt to create the interest to pay off all previous debt. If consumers stop borrowing then governments must fill the gap to keep the music playing, bloating the debt burden of future tax payers.

2. The modern system has made banks the centre of the financial universe, holding us captive to their self-interest. They are now masters of our collective destiny.

3. The system relies on trust in government decreed fiat currency, and all previous historical experiments in fiat currencies have resulted in disaster.

4. It has created never-ending inflation which is a hidden tax on the purchasing power of every unit of currency in your wallet, every day, so why save?

5. It encourages reckless government spending, and mountains of corporate and personal debt.

6. It is bankrupting the supplier of the global reserve currency, the USA. And it enslaves the middle class in lifelong debt and crippling taxes, while enriching global elites.

Because of these inherent instabilities, our global financial system is now coming to the end of its lifespan, a lifespan that has mirrored the rise and rise of atheism in Western culture. We are reaping what we have sowed. In the next section I will shine a light back on two significant episodes in this grand fiat experiment, two episodes when the global financial system both just missed an iceberg, and grazed an iceberg. I will then shine that same light onto the course in front of us out to the year 2020, to see when, how and why the rusty, overloaded old ship called SS Fiat will finally go under when it hits the next iceberg head on.

THE ASIAN FINANCIAL CRISIS OF 1998

In the year of 1998 I made a lot of money on the futures market trading the rebound from the Asian Financial Crisis. I knew little of its causes, so it was dumb luck that made the money. It was a classic bankruptcy of nations, triggered by the huge debts and then depreciation of the Thai baht in July 1997. The unfolding of the events of 1997-98 below will serve as lesson number one in what is coming around the end of this decade.

After the fall of the Soviet Union in 1989, a new era of globalised investment and speculation was born. A lot of hot investment money flowed into Asia. In Thailand, investors borrowed in US dollars with its low interest rates and poured massive amounts of funds into real estate, creating an unsustainable boom. The Thai Baht had been pegged to the US dollar for 14 years, but now this link had turned into a noose as the export economy was uncompetitive and the country struggled to pay back a mountain of loans. The currency peg was breaking down, foreign debt was astronomical and the economy was bankrupt. On July 2nd, the government suddenly devalued the currency 20%, lenders instantly suffered colossal losses and started taking their money out of the country, exasperating the problem.

Indonesia and Korea had followed similar economic and investment policies to Thailand, and quickly collapsed as well. On August 14th, Indonesia also broke its currency peg to the dollar and its currency also went into free fall. There was blood on the streets as riots erupted and President Suharto was eventually forced from power. The Asian financial crisis of 1997 was born. The International Monetary Fund (IMF) eventually stepped in with emergency loans to all three countries as systemic banking collapses, stock market crashes and violent social unrest unfolded. The IMF imposed strict monetary discipline, but it was saving the banks and bondholders at the expense of ordinary citizens.

Global investors no longer trusted emerging economy exchange rates. They wanted their money back. Markets were skittish. On October the 27th, 1997, the Dow Jones shook and fell 557 points. However, after the initial storm, everything seemed fine again for six whole months. But under the surface funds began to be repatriated to the west on a massive scale. It was only a matter of time before the contagion re-emerged.

The next year the crisis erupted again in Yeltsin’s Russia when the once mighty Russian bear defaulted on its debt and depreciated its currency on August 17th, 1998. Hot investment money had flooded into Russia after the collapse of Communism. However the immaturity and corruption of the Russian leadership meant that mishandling of these funds was inevitable. (It is from this time of abject humiliation that Vladimir Putin was able to ride to power, promising a new golden age of Russian pride and the rest is history).

From there the contagion spread to a star of American finance, Long Term Capital Management (LTCM). LCTM had vast exposure to Russian and Asian debt. LTCM had been the darling of Wall Street for six years, producing returns the envy of the street. However its secret was to use huge leverage, take the opposite side of a partner who needed money quickly and was offering a discount, and to double down on bets if they went against their expected outcome in the short term. This worked fine until the Asian Financial Crisis erupted. By April of 1998 the LTCM monthly return had strangely turned negative. No problem, they simply doubled down. By August they had over a trillion dollars in total exposure to trades that continued to sink. Then came Russia and everybody wanted their cash.

At the end of August, LTCM was miraculously still standing and still honouring redemptions. However, it had chewed up to 50% of its capital reserves. LTCM’s contracts locked counterparties into the terms LTCM dictated, so no counterparty could renege on its contracts. By early September, banks across Wall St realised, to their horror, that they were locked in to a financial seatbelt with LTCM. What if LTCM losses caused a bank to fail? What if my bank was exposed to that bank? Now Wall St banks feared each other. The US banking system began to seize up. The oil that greases modern finance, inter-bank trust, was gone. On September 17th, LTCM made a discreet and desperate phone call for help to the US Federal Reserve.

The IMF had a mandate to bail out Russia, Thailand, South Korea and Indonesia, but not to help private hedge funds like LTCM. So the Federal Reserve and the US treasury began to ring-fence LTCM before dominos began to fall all over Wall St, and around the world. Over an intense six day period from September 23-28, 1998, Wall St and the Fed cobbled together a 16 bank consortium that delivered a $4 billion bailout. But not before two Wall St banks almost destroyed the deal twice in the name of predatory self-interest. The Fed also cut interest rates twice so the 16 reluctant banks got the message the Fed had their back. The banks were not really bailing out LTCM, but themselves. The Fed did “whatever it takes”. Wall St got the message and the global economy was saved, by days.

Shockingly, in the aftermath of this first crisis that almost sunk the world’s fiat monetary system, US regulators did exactly the opposite of what they should have done. They should have sent all derivatives to a public exchange where they were visible. They should have enforced a reduction in leverage. They should have banned banks from trading in derivatives. They should have increased transparency in balance sheets. They should have increased capital ratios for all financial institutions so they could survive future crises. However, Alan Greenspan and his two friends, the “committee to save the world” as Time Magazine called them, did the opposite to all of these, against the explicit advice of the head of the Commodities Futures Trading Commission, Brooksley Born.

Why did they do the opposite? Because Wall St, and Wall St banks in particular, own Washington’s politicians. Here’s the proof: In 1999 they successfully lobbied for the repeal of the sixty year old Glass-Steagall Act, which separated risky investment banking from safe retail banking. Banks were, for the first time since the Great Depression, back in the derivatives business. In 2000 Wall St banks also successfully saw the repeal of laws that used to make many types of derivatives visible on balance sheets. By 2004, global banking rules were allowing banks to leverage up their loan capital ratios to 50:1. This witch’s brew of declining financial regulation led directly to the 2008 Global Financial Crisis!

There are many lessons an astute investor and student of history can learn from the near-disaster of 1998. Here are a few:

1. Some institutions were now too large to fail. They would bring down the whole fragile Western financial system if allowed to fail. They have to be bailed out. As I write, this is now leading to creeping government control of many of the world’s systemically important financial institutions. If they are too large to fail, they must be controlled.

2. Wall St banks hold a financial gun to the head of Washington lawmakers. This is true of almost any country because money is power. Bankers will always get their way and will always act in self-interest…until they all go bankrupt from that self-same self-interest in the next crisis that will lead to a global depression and a resetting of the rules. This culture of greed sows the seeds of its own eventual destruction. It is simply a modern expression of the spirit of mammon condemned by Jesus (Luke 16:13).

3. The new era of derivatives that emerged in the nineties was opaque, unregulated, highly leveraged and inherently risky. It still is. As I write, there is now a quadrillion dollars, or a thousand lots of a trillion dollars, in derivatives contracts outstanding. This is a ticking time bomb that has already gone off twice.

4. Bail outs and excessively low interest rates were to be the future solution to bankrupt financial giants. Governments should have been letting them go. This was called the “Greenspan Put”, after the then head of the Fed, Alan Greenspan.

5. When financial contracts double in size, they multiply exponentially in complexity. Therefore the risk of default also rises exponentially.

6. When governments and bankers destroy the financial system, people grab their pitchforks and come after them. Revolutions start during financial turmoil and desperate people do desperate things. Multiple central bank chiefs have simply passed the buck on to their successor so they don’t face the music on their watch.

Now let’s move on to the next global crisis, born out of the 1998 debacle, entirely avoidable, still with us, and simmering in the background.

THE GLOBAL FINANCIAL CRISIS OF 2008

Another decade, another financial disaster. If you have seen either of the movies “The Big Short” or “Margin Call”, you will have some idea of the size of the mess the Western world fell into during 2008. I spent the Christmas holidays of 2007-8 in Perth, Western Australia, visiting my brother and his family. When in the city on the last business day of the year I could hear massive corporate parties going off all over the CBD. Pubs, restaurants, corporate offices and practically any public venue was full of mostly men in suites celebrating another bonanza year. In retrospect I realised that this is what the bell at the top of a boom sounds like, corporate celebration!

How did we get there? Simple; too much real estate debt built on artificially low interest rates. Interest rates had been lowered after the dotcom boom and bust of 2000, and never returned to normal. The signal to punters was clear, “go for it, debt is too cheap”. It was far too cheap and the result was a disaster born of central bank incompetency. Baby boomers the world over had paid off their homes and began to venture into real estate investment in a big way. The working class were conned into home loans they should never have qualified for. Anyone could get a house loan. My wife was a mortgage broker for a year during this time and it was scary to see who the banks would lend to, via their subsidiaries. Global house prices went through the roof, doubling and tripling in a few years. I used the boom to buy an investment property, sold it three years later, and paid off our mortgage. I will explain that experience in more detail at the end of the seminar.

The 2008 crisis was triggered by securitised subprime mortgages. This was a new form of real estate derivative that bundled many mortgages of differing quality together, certified them with a AAA credit rating, and then sold them on to unsuspecting third parties. From 2001 until 2007 the value of derivatives, led by sub-prime securities jumped 500%. The stock market also exploded on cheap debt, as it is also doing now. Homes became ATM’s for a spending binge and savings rates actually turned negative for a while. China supplied the cheap goods we bought with this new source of cash. From India to Indiana, from Stockholm to Sydney, the whole world collectively binged and artificially boomed. However, the party was on borrowed time as well as money. We were heading toward another iceberg.

Here’s how it all unfolded. In March of 2007, The Fed, asleep at the wheel as usual, naively said that the mortgage market was performing well! But by late 2007 several international banks were already suspending redemptions in funds that specialised in mortgaged-backed securities and TV analysts were laughing at the Fed’s incompetence. Liquidity was once again evaporating behind the scenes. It was obvious for those who had eyes to see. In January of 2008 the Fed again proclaimed their blindness by saying they were “not currently forecasting a recession”. It was calm for two more months, and then Bear Sterns collapsed. In May of 2008 the US secretary of the Treasury, Hank Paulson declared that “The worst is behind us”. On June 10, the Fed once again said “The risk that the economy has entered a substantial downturn appears to have diminished over the past month or so.” But the stock market continued to fall relentlessly. It was calm for another two months, then Fannie Mae and Freddie Mac, two corrupt government-backed mortgage lending institutions declared bankruptcy, and were bailed out by the US government.

That’s when the snowball began to really gain momentum. Below is a roll call of events from that point on that illustrate just how close the world came to complete financial meltdown. When inter-bank trust is broken collapse comes very quickly:

September 12-14th: All major players in American finance meet to try to save Lehman Brothers, a bank that had refused to join the 16 bank bail-out of LTCM ten years earlier. September 15th: England’s largest mortgage broker is “rescued” by Lloyds bank. September 16th: The US Fed loans $85 billion to AIG. Two days later it increases lines of credit to $185bn for all banks. September 17th: Lehman Brothers is abandoned by the Fed and files for bankruptcy. September 19th: The Fed agrees to take on all toxic debt from all banks if they wish to sell. September 25-29th: Washington Mutual and Wachovia banks collapse, and the Fed establishes a $330 billion line of credit with most other central banks around the world…

…October 3rd: US congress passes a law to release $700 billion to bail out banks. October 7th: The US Fed announces a depositor guarantee of $250,000 per account. October 6-10th: Another $37.8 billion is loaned to AIG, and Iceland’s banking system completely collapses. It’s also the worst week for the US stock market in 100 years. It’s also the week eight central banks cut interest rates by 0.5%, then keep cutting and cutting to zero. Global fiat finance was spinning totally out of control. The ship was sinking. The RBA of Australia cut interest rates that week by a full 1%, and then another 3% over the next five months. A run was developing in Bank West in Perth, and several more US banks. Armaguard was scrambling to supply banknotes. People were hording cash. Talk-back radio was being asked “is any bank safe?”

The proverbial had hit the fan and by Friday the 10th of October, the world was on the brink of collapse. We had hit an iceberg. Emergency meetings were held all over the world during that fateful weekend, but especially in New York and Washington with phone links to many other countries. On Sunday, October 12th, in response to a run on Bank West the week before, the Australian government declared all bank accounts up to $1 million guaranteed by itself. On Monday, October 13th, the Fed extended almost unlimited lines of credit to foreign central banks and domestic banks. The next week the British government bailed out the Royal Bank of Scotland, Lloyds bank, and HBOS. From this point on the crisis began to settle, but not before millions of people lost their jobs and their debt-fuelled fake fortunes. The Fed, using limitless fiat money had restored a fragile trust in the system. The ship was stabilising. As if to highlight the purpose of all that money, the governor of the Reserve Bank of Australia, Glenn Stevens, said in September 2016 that these combined actions “calmed depositors, which is 99% of what matters…I hope it was a once in a lifetime event.” Hmmmm.

The Fed had bailed out the world, but at a huge cost. If it hadn’t acted so boldly the world’s financial system would have seized within days and hundreds of millions of people would have been instantly without employment, holding useless credit cards and bank statements. It would have been a disaster unlike any other in world history.

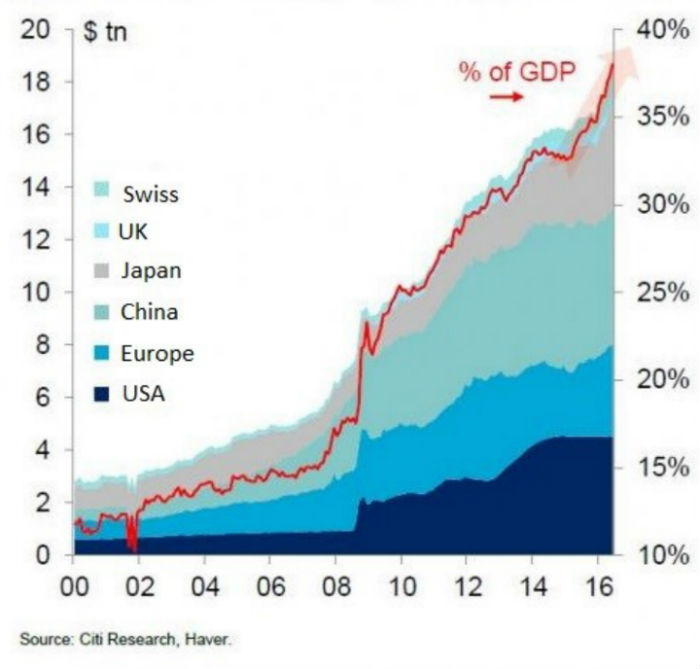

It was only in retrospect that we discovered the extent of the emergency loans handed out by the Fed to keep the world’s economies and banks afloat during that fateful week. In 2010, we found out that the Fed had to give $5 billion in emergency loans to two of Australia’s largest banks, National Australia Bank and Westpac, to keep them from bankruptcy. It was only in 2015 that the US Special Inspector General itemised the entire bailout and found the total Fed commitment was $16.8 trillion US dollars, an amount never declared at the time for fear it would undermine confidence. This money was created out of thin air by the US Fed, and pumped into the arteries of a dying global banking and financial system. Other central banks likewise pumped billions into their economies.

So, where is all that money now? Over $US 10 trillion was paid back to the Fed and cancelled. However, the Fed’s balance sheet is now five times what it was before 2008. By 2016, collective central bank balance sheets around the world had grown to over 40 percent of global GDP from just 15 per cent prior to the global financial crisis, with no sign of ever shrinking back to their original size! The bloated balance sheet of the Fed, ECB and Bank of Japan are now ticking time bombs.

After the crisis had passed the US Congress once again decided to clean up Wall St banks with new legislation via the Dodd-Frank Consumer Protection Act. However, it was sent from congress to several government agencies for final drafting. That’s when bank lobbyists gutted it. It ended up as a mixture of genuine reform, pseudo reform, rubbish and non-essential matter from lobbyist wish-lists. Another wasted opportunity.

What were the lessons learnt from this near-death experience? What can you take into your future decision making?

1. Governments have a vested interest in talking down any problems that are emerging. Trust in banks is the linchpin to the whole system. When a public servant has to say all is well, it is a signal that it is not!

2. Central banks will just make it up as they go along, stumbling into the next policy move in reaction to what they clearly did not see coming. They are blinded by their out-dated economic models. Don’t expect them to have the answers next time.

3. The one tried and true reaction to a financial crisis is for central banks to lower interest rates and print money. This has now become a drug from which there is no escape. The next crisis will see much more of the same, with the distinct possibility that Western central banks themselves will go the way of Thailand, Indonesia, South Korea and Russia in 1997-98… bankrupt! Severe falls in all currencies compared to gold, such as we saw in the 1970’s, will be the evidence of this.

4. People will always look for cash in a crisis, destroying banks in the process. It is instinct to move to higher quality forms of money when fear for the future is in the air. Those that have already secured access to quality forms of money will do very well in the next crisis.

5. The system is very, very, very fragile! Once shaken, tremors come in waves, building to a climax. There is plenty of warning of the final catastrophe.

6. The economy determines politics, not the other way round. The events of 2008 put Obama in the White House. Governments around the world fell like dominoes.

7. After all the lying, cheating and swindling that created the subprime mess in the first place, not a single bank executive outside Iceland has been sent to jail! The banks own the system and are happy to pay billions in fines, but never pay a personal price for their actions. This creates a form of moral hazard that must be rooted out.

8. Unfortunately regulators to this day do not see default risk, only the risk of incremental movements in underlying instruments in two-way contracts, such as interest rates and currencies. So, when the next crisis hits regulators will still not have clue how to handle massive defaults they were not expecting, and will do the one thing they have always done, print money and give it to banks.

If only I had known, in Perth over Christmas 2007, that the world was about to change dramatically, what fortunes I could have made. Ditto for all of us. Yet it’s only been ten years and already our collective memory has lost touch with the severity of those events and the potential impact that year could have had on all our lives. The signs are everywhere that we are about to enter another storm. Why can so few of us see it coming?

THE COMING CRASH OF 2018-19

Which brings us to the present. Where are we at, and what is coming? How can you prepare? How can you be safe? This time the masters of the universe will not be able to save their precious fiat financial system from utter collapse. It is now early 2018. Let’s now look at the signs of what is coming.

We are now 104 months into the latest economic expansion post 2008, the third longest in history for the USA. Economic expansions since WWII averaged only 61 months, so we are overdue for major “recession” any time now. Then there are the financial bubbles the US Fed keeps blowing. The emergency lowering of interest rates initiated as a reaction to the LTCM crisis led to the dotcom bubble. The dropping of interest rates from 6% to 1% after the dotcom bubble bust led to the housing and stock market bubble of 2008. The artificially low interest rates since 2008 have led to an “everything bubble”, which includes property, stocks, bonds, national debt, personal debt, central bank debt, emerging market debt and corporate debt. This bubble is about to pop. When the everything bubble and another once-a-decade existential financial crisis both smash into a world drowning in debt, you have a recipe for a global depression. That’s the iceberg I am talking about. You can’t kick the can down the road forever, one day you will run out of road.

This section will show you why I just used the word depression. It is definitely coming and I will show you how to prepare for it. The disasters of 1998 and 2008 were not the main event. It is still in front of us, but not far away. The consequences of each crash are getting larger. It’s as if ever larger tremors are announcing the coming of a major earthquake, or our ship is entering an iceberg pack and they are getting bigger. In 1998 banks were called on to bail out LTCM. In 2008 central banks were called on to bail out all banks. In the near future central banks and nations will need bailing out. But by who?

Which leads us to a lesson on who now runs the world’s finances. The G20, the European Union, the UN security council, the major central banks, the Bank of International Settlements, the IMF, the globally significant/too big to fail financial institutions, transnational business and ultra-wealthy investors run the world as a loosely connected club. At the end of the day there are vast political and religious differences between them, but they are united by fiat finance and the artificial power that comes with it. The 6,000 people that run the world, most of whom attend the Davos conference each year, who also control the G20, run the IMF, preside over the UN, lead the big banks, the sovereign wealth funds and big business have a huge vested interest in the current financial architecture. It’s their system, their baby, and they benefit the most.

They control the media, academia and the neo-liberal humanist political consensus, a consensus of quasi-free markets (but which favour multi-national businesses, not small business), international trade deals that result in a continual loss of national sovereignty, increasing international migration, Keynesian economic policy, big government, the welfare state, floating fiat currencies, debt-fuelled economic growth, nations ceding power to their transnational institutions, fractional reserve banking, and soft-sell socialist control over our lives.

These people are not part of a suspicious one-world-government conspiracy, but rather just a convenient merging of interests with actors coming and going. It’s how all elites have always run things. In first century Israel the religious elite had used religion as a mask to grab total financial and political control over the Jewish people. Attacking them was the reason why Jesus was executed (Matthew 23:1-39, John 11:50). God hates human manipulation of other humans. We are to serve, not control.

However, at this point in time, the global elite all know something we punters do not. They know the current system, their system, is on its last legs and is close to collapse. They are all scrambling to prepare for the inevitable iceberg. They have the most to lose if the system sinks. They fear the faceless mob armed with their figurative pitchforks! So they are planning for the demise of the US dollar as reserve currency and a transfer of that status to the IMF’s own unique currency that has been in existence for some 47 years. It is called Special Drawing Rights, or SDR’s.

SDR’s have only been used four times, the last being in the depths of the 2008 crisis. There is now approximately, SDR204 billion in circulation, worth about $US285 billion. This evolution away from the US dollar and to the SDR is part of their plan for world money, part of an attempted guided evolution away from national structures to preferred supra-national structures, such as those the elite already control. Because the IMF does not run structural deficits, they believe SDR’s will be the perfect solution to Tiffin’s Dilemma. Belgian economist, Robert Tiffin, rightly pointed out in 1960 that the US government would eventually go bankrupt through having to run deficit budgets to supply the rest of the world with its reserve currency. Once SDR’s have replaced the US dollar as the global reserve currency, the IMF will then function as the central bank for the world’s central banks. That’s their plan.

The global financial elite are also planning for a short term closure of all banks so they can be recapitalised using depositors savings instead of taxpayer’s funds. This will be called a mass “bail-in”. More on that in a minute. This might sound new and bizarre to you but bank closures, bank holidays and bankruptcies were common practice before the modern Bretton Woods/fiat era, and before the recent era of bail-outs. Bail-ins are going to be used again in the next crisis as a kind of bumpy crash landing for the system.

But I believe the elites will fail and the system will crash and burn completely. They will fail because their fiat financial system is built on the quicksand of fractional reserve banking and ever-increasing debt as the road to ever-increasing global economic growth. All such systems, whether biological or man-made, reach natural limits and this system is reaching its limit. Cracks are appearing in unexpected places. The frightening developments listed below are some of these cracks:

1. As mentioned above, central bank balance sheets have not shrunk since 2008, but have ballooned to over $US 20 trillion. Stinking toxic debts, debts that banks didn’t want and the central banks gladly took on, still sit there like the submerged 5/6ths of an iceberg. The ECB and the Bank of Japan have actually been actively expanding their balance sheets over the last few years in an effort to pump-prime their forever-stagnant economies. Their economic ships seem to be broken down and adrift mid-ocean. What were once unprecedented emergency measures, are now considered normal. Who will bail out the central banks?

2. The 2008 crisis was a debt crisis, and was fought with more debt. It was like putting fire out with oil. Total global debt levels are now some 30% higher than in 2008, at about $US240 trillion, with $58 trillion in the government sector as global governments, in true Keynesian form, pick up the slack from a reduction in debt from the corporate sector and stagnant debt in the household sectors. Emerging markets such as China have especially seen a massive increase in corporate debt, government and personal levels.

{kind=link}

3. The derivatives obligation of global financial institutions is now over $US1 quadrillion. Remember how derivatives exploded onto the scene in the 1990’s, causing the LTCM disaster, and then caused another iceberg in 2008 via the subprime mess? Well the mountain of promises has just kept growing. This link gives you a visual idea of the sheer size of the problem. It is now beyond our imagination at over a thousand trillion US dollars. Central banks are highly sanguine about this number as they only see risk in the margins of underlying security movements, not in cascading defaults tearing down the whole pyramid, as has already happened in 1998 and 2008

4. The US government faced a significant crisis of confidence in January 2012, when lawmakers would not increase the debt ceiling limit from $US16.39 trillion dollars. Gold reacted by rapidly spiking to over $US1900 and the US dollar tanked. There was a real and present danger of America defaulting on its debt. A last minute compromise saved the day. However, thanks to Obama and Trump’s big spending policies, six years on the debt now stands at over $US20 trillion and no one in Washington takes the ceiling seriously. In fact, under Trump’s infrastructure spending drive the debt is exploding to far higher levels in the next few years. This could create an existential crisis for the US dollar. Tiffin’s dilemma is unfolding before our eyes. Another time bomb is ticking.

5. To contain the interest payments on this astronomical debt level, and to stave off a deflationary nightmare of 1930’s proportions, the Fed reduced interest rates to virtually zero from 2008 until late 2015. This socialist distortion of normal market signals has resulted in a plunge in the velocity of money as banks cannot make profits through loans at these rates. Money has piled up on bank balance sheets, and flowed into emerging markets and stocks via the so-called 1%, the ultra-wealthy, who can get access to this near-free money. It has also gone to corporations who are borrowing money to buy back their own stock at the current rate of US$1.2 trillion a year, as of February 2018.

6. Because interest rates are artificially low, payment on the US government debt is “only” about $300 billion, or 7% of tax revenues. However, according to the Bank of International Settlements, we are now in a long-term rising interest rate world. Every 1% rise in interest rates increases the US government’s annual interest payment by around $200 billion. Market rates on the bell-weather US ten year bond rose almost 1% in just the six months from September 2017 till February 2018. The market smells inflation and tighter monetary conditions coming.

7. These tightening monetary conditions are a direct result of the US Fed now fully engaged in Quantitative Tightening (QT). This means they are taking money off the market and destroying it. They are desperate to shrink their balance sheet before the next crisis, after exploding it over the last ten years. They began QT at $US20 billion a month. By October 2018 they will be shrinking their balance sheet, and therefore the US money supply, at $US50 billion a month. This is an annualised reduction of $US600 billion a year on a $US4.5 billion balance sheet. The Fed is in a race against time to shrink its balance sheet before it has to expand it again in the next emergency. If the Fed has to issue another $4 trillion in bonds to rescue corporate America in the next crisis on top of an existing $4 trillion balance sheet, all confidence will be lost and the US dollar will collapse completely, ending its reserve currency status and their global military hegemony, in the most undignified way possible.

The Fed carries out its QT by not replacing expiring bonds. Fewer bonds in the market mean higher interest rates. It was the excess supply of bonds relative to demand from Quantitative Easing (QE) that kept rates far too low for far too long. QE is simply electronically “printing” money out of thin air and sending it into circulation. QT is the opposite. The Fed knows they will have to engage in massive QE again when the next recession hits, and they also know they are way behind where they need to be. They were lazy, they dropped the ball.

8. This is also why the Fed is now, in 2018, desperately raising short term interest rates at a quarter percent each and every quarter. Once again, they should have started this years ago, but the Fed is run by timid PHD academics, who are on record as saying they don’t believe there will be another bank run in our lifetimes! When their recent new-found financial prudence is combined with Trumps demand for funds to support a $US 1.2 trillion annual deficit, the result could be interest rates hitting 4% very quickly. This means both the Fed and the government will be draining a combined $US 1.8 trillion from the American economy by the end of 20218.

Imagine what a doubling of interest rates will do for the repayment schedule on the US government debt, or the stock market, or the housing market, or the bond market, or the corporate debt market, or emerging market debt denominated in US dollars? What will be the flow on effect in the global shale oil fracking industry, which has a combined US dollar debt of over $5 trillion?

9. Over in Europe, the EU has been even more financially promiscuous. The 2008 crisis saw Spain, Italy, Ireland and Greece collapse and cry out for help. Their debt sodden economies could not stand the global downturn and default was in the air everywhere. However these nations were stuck with a euro run by Germans, so they could not devalue their currency as the Asian countries did in 1997-98. The European Central Bank (ECB) decided to do “whatever it takes” buying up anyone’s debt to solve the problem. Electronically printing trillions of euros (QE) and buying up unloved toxic debt in the process.

However, even then Greece still failed completely due to its crazy culture of welfare entitlement and international lenders had to take a haircut. Spain and Ireland have partially recovered, while Italy is still on life support to this day. No one but the ECB buys their bonds and no one would want them. The ECB balance sheet has exploded again in the last five years, after the US central bank eased back on its own QE. With its aging demographics, rigid labour laws, and high youth unemployment levels, Europe will suffer terribly in the next downturn.

{kind=link}

10. Then there was the experiment called Cyprus. Long known as a launderer of Russian money, Cyprus banks collapsed in 2012-13 along with Greece. After the debacle of Greece the ECB decided on a new and novel idea. Instead of a bail-out where bank creditors and taxpayers footed the bill, Cyprus became a bail-in experiment, where depositor’s funds were confiscated and used to recapitalise the banks. This worked, and has now become the template for the next financial crisis. Bail-in laws have been enacted in all major nations over the last few years. The G20 summit in Brisbane, Australia, was the place and time where this was agreed upon as a future tactic for handling a financial crisis. In fact, the G20 has now become the de-facto governing board of the world. It’s where all major global policy decisions are made. So, the next crisis will see our bank accounts and financial assets frozen on a global scale. I predict there will be blood on the streets of Western countries in reaction.

11. Still in Europe, and we have now seen something truly extraordinary, something never before seen in 5,000 of financial history…negative interest rates! How did this happen? How is it possible? With inflation at close to zero, zero interest rates do not provide enough incentive to take money from the bank and spend it. The solution, coming once again from the genius of central banks, was to create a new concept, negative interest rates. Depositors were now being charged interest instead of earning interest on deposits. The solution for large institutions was to swap over to stocks, real estate or bonds. This was exactly what the financial puppeteers wanted. It’s another sign the current fiat monetary system is starting to destroy itself.

12. This bizarre move has gone hand in hand with a war on cash. Negative interest rates incentivise people to hold cash outside the banking system. Right on cue there has been a herding of the world’s citizens into electronic forms of commerce, increased suspicion and reporting on cash transactions, and a removal of large bank notes from Europe and India. When cash finally disappears, and it will, there can be no run on a bank in an emergency, no recourse against whatever is decreed by the global financial elites, or governments, or banks. The G20 has already decided that in the event of a financial collapse, deposits will be converted to bank equity. That policy assumes the money is stuck at the bank. Precious metals and other real assets are the only safe haven in such a situation.

13. The global recovery since 2008 has been unusually mild compared to previous global expansions. In many countries it’s as if they live in a 2008 Ground Hog Day, there has been no growth, just stagnation. But some parts of the world have boomed, one in particular. Since 2008, China has accounted for 50% of all global economic growth. Since you now know that all economic growth is only possible because of a growth in debt, you can understand why this phenomenal growth is unsustainable. It’s because China has increased its debt from $7 trillion to $28 trillion since 2007. Of that figure, over $US5 trillion is classic central bank pump priming QE by the PBC, the rest is corporate and personal debt. China’s government debt to GDP ratio is now far higher than America’s and is approaching that of Japan. In the end, ghost cities, new silk roads and mega infrastructure projects will be completed, then what? Australia stands to lose the most when China falls as China accounts for about 35% of its exports. We are tied to China at the hip. Studies have shown that Australia’s national income will drop by at least 10% when China hits its own debt iceberg.

WHERE ARE THE LIFE JACKETS?

In this section I give you what I believe will be a rough idea of how international events will unfold, and how you can prepare for them.

When economies flourish, democracy flourishes. When economies collapse, people grow poor and desperate. That’s when dictatorships flourish. We have seen this over and over again, with the most obvious examples being the collapse of Weimar Germany and the rise of Hitler and the collapse of Russia and the rise of Putin. When the next crisis hits, ultra-nationalism, fascism, socialism, and even communism will stage a comeback. People will yearn for a strong man or woman to solve their problems. Any order will be better than disorder.

Capitalism will be blamed for what will essentially be a crisis of crony miss-management, central bank bubble-blowing, fiat currency-based, debt-based, elitist neo-liberalism. Freedoms will disappear, traded for security. Trade protectionism will rise. Economic nationalism, as we have started to see in England and America will accelerate. Militarism will rise significantly and wars will erupt. Be prepared for this. It was the story of the first 45 years of the 20th Century, so it is perfectly feasible.

The more complex a system, the more profound its collapse. The global economy is now a hideously complex connection of contracts and currencies, derivatives and debt, trade and transnational corporations. It is the systemic instability of this system that will destroy your wealth, not an individual catalyst. Watch for the following clues of rising instability:

1. Watch for rising interest rates in the US 10 year bond. Interest rates rise when funding is short and inflation is on the horizon. The best place to watch for movement is to keep an eye on the US 10 year bond rate.

2. Watch for defaults in second tier financial institutions around the world, especially in globally significant emerging markets like China and Russia.

3. Watch out for sharp and unexplained negative currency movements in countries with huge debt burdens.

4. Watch out for a spike in the London Inter-bank Overnight interest Rate, or LIBOR. This is the interest rate at which banks lend to each other. When it spikes, banks no longer trust each other. It forewarned of trouble in 2008.

5. Watch out for a blow-off top in stocks as the last of the smart money sells to the last of the momentum chasers, the dumb money.

6. Last, watch out for politicians saying smooth words of comfort when things go a little wobbly.

7. Watch out for a pause in the raising of official interest rates and talk of looming QE

In any crisis wealth does not disappear, it just changes hands from the foolish to the wise. If you aim to preserve wealth in the next crisis you will probably end up with more wealth than you expect. Prepare wisely and you will pick up bargains from desperate sellers. A friend of mine lived through the Argentinean financial crisis of 2000. He told me that house prices dropped 90%, when the government confiscated everyone’s bank accounts to pay the national debt they had just defaulted on. Houses dropped to the level of cash. Those who had not trusted the banks or government became wealthy overnight.

The best way to prepare for a very uncertain future is get ready to grow your wealth outside the fiat currency system. To do this you must look to the stores of wealth that have stood the test of time; good land, the best art and gold are tried and true repositories of real wealth. They are tangible wealth, not fiat wealth. This is the combination that has kept the great families of Europe afloat through the many centuries of turmoil that have beset that continent.

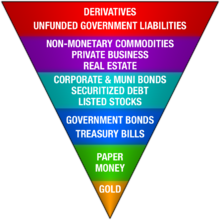

In the next crisis there will be a rush from low to high quality stores of wealth. Consider Exter’s Pyramid below, named after its creator, John Exeter, a former governor of the Federal Reserve. The poorest and largest form of wealth is derivatives, at the top. That’s why they cause problems in a crisis, no one wants them. From there we move down to small business, real estate and government bonds, which will devalue significantly in the next crisis when business and governments, as well as banks fail. Because real estate is a debt based market it will suffer as people avoid debt. Near the bottom we have cash and then gold at the very bottom.

For five thousand years gold has been a reliable, portable, enduring and simple store of value. It is independent of government decree or control. It has been ridiculed by the fiat monetary elite for forty five years because it is the mortal enemy and only major competitor to the US dollar. However, gold is money and always will be. That’s why the world’s central banks still hold over 35,000 tonnes. Central banks know gold is money. They just don’t want you to know.

At the moment, because of the dominance of rigged futures markets, gold trades only at its commodity value. When the next crisis hits, it will trade once again as money, and at multiples of its current price. Those who have gold will make the rules and control the architecture of the next monetary system that will rise from the ashes of the next crisis. This is why China is importing over 2,000 tonnes of gold a year, almost equal to the entire current global production outside of China.

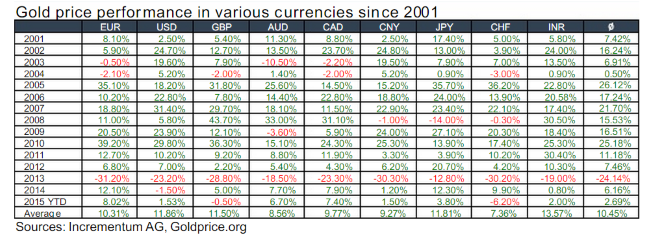

Since the year 2000, gold has been rising at an average of 10.45% against a basket of the world’s major currencies. It is set to rise a lot faster in the years ahead as governments try to inflate away their debt and hobble their interest rates below the inflation rate. Combined with a shrinking production rate for gold around the world, the stage is set for far higher prices. The most famous banker in American history, J.P. Morgan once said “Gold is money. Everything else is credit.” I agree.

THE ULTIMATE LIFE JACKET

Economics, taxation and finance are expressions of individual and state sovereignty. However ultimate sovereignty belongs only to our creator (Genesis 1:1, Matt 28:18). If you doubt me then read this link. The reason why our Western financial system and culture is now in a downward economic spiral is because we have abandoned our Judeo-Christian worldview, the foundation of Western civilisation and its economic heritage, sometime in the last 100 years. The result will be a continual drop in wealth and prosperity into the future as our selfish lust for me-first, spend-now-pay-later lifestyles and debt blows up in the form of massive national debt defaults and currency crashes in the coming years. There is an iceberg dead ahead, but most people are still partying on the deck of the good ship Titanic.

There is room in the human heart for only one lord. That place belongs to Jesus, the creator of the universe. However, money is currently the most worshipped god on earth. Its worship covers all cultures, all religions and all worldviews. The rich young ruler worshipped this rival deity and walked away from Jesus (Matthew 19:21). Zacchaeus renounced his worship of money and it was considered salvation (Luke 19:8-9).

The Genesis account of the fall of humanity teaches us much about the true nature of economics, finance and ultimate sovereignty. The following list of the economic implications of the first three chapters of Genesis is instructive:

1. God is the boss. He is sovereign and the employer of humanity (Genesis 1:1).

2. God privately owns everything, including us. Private ownership is therefore a very important Biblical concept (Psalm 50:10, Colossians 1:16-17).

3. God has leased the planet to us. We are stewards and foremen over creation. Dominion was our first assignment (Genesis 1:28-30).

4. The first sin was economic. It was theft from a tree, theft from God. In all our sinning since, we have been thieving from God.

5. God has placed performance standards and accountability in creation. Adam and Eve failed the test of dominion through submission. The workers tried to sack the boss, take over the estate and create a paradise where all were equal to God. For this little insubordination they got fired!

6. Because the fallen nature of humanity centres on the will to personal power, God had to decentralise power and responsibility through a curse on creation.

7. Scarcity in nature is therefore deliberate, placed there so that humans have to work to live. Dominion has become much harder now, though still possible. Fiat currencies are but one attempt to avoid the curse of scarcity.

8. Humans are now selfish by nature. (Luke 12: 16-21).

9. We are also slaves to sin in need of forgiveness and a redeemer. A redeemer is someone who can buy a family member out of slavery (Colossians 3:13).

Jesus talked more about money than any other topic except the kingdom of God. This was because money is a window to our soul and our soul is supposed to be the throne room of the king of all kings, the president of all presidents and the prime minister of all prime ministers. It matters little whether you are a government treasurer handling billions of dollars, a businessman handling thousands, a mother struggling with grocery money, or a village farmer who only sees money when she comes to the market. All of us develop an intricate value system based around the money we handle and what it means in our lives. This attitude becomes a deeply ingrained part of our worldview.

Money has a dark side to it that Jesus continually addressed. He attacked the selfish rich (Luke 6:24). He suggested we seek treasures in heaven before treasures on earth (Matthew 6:19). He warned us of the dangers of greed (Luke 12:15). He drove the moneychangers out of the temple (John 2:12-16). He also challenged us to choose between loving money and loving God (Luke 16:13). It is this last point that is most important in this discussion on economics. When Jesus spoke about loving money in Luke 16, He actually used the word mammon, not money. Jesus deliberately used an old Aramaic word that means money personified, deified and worshipped. By using the word mammon, He was declaring money to be a rival god. He was giving it personal and spiritual character. He was telling us that behind money are very real and powerful spiritual forces.

Money, contrary to popular humanistic dualistic thinking, is not morally neutral. It has a life of its own that can take over our heart. It has taken over the hearts of Wall St, Washington, the city of London, all our banks, big business and even millions of humble lotto players. We have worshipped mammon and are about to pay the price for worshipping a false god. It is my prayer that the disaster that lies before us will be a turning point for the Western world, bringing it back under the sovereignty of Jesus Christ. Only then will governments and individuals find the solutions they will be seeking.

Let me illustrate and finish with this story. In the year 1999 I bought a house with an 80% mortgage. Knowing the Biblical standard is to live a debt-free life, I sat on the driveway one night and asked our creator Jesus to help me pay off my 25 year mortgage in 5 years. Using hard work and wisdom I was able to increase the value of my home, buy an investment property the month they took off in the year 2000 and sold it three years later at double the price. My home was paid off in 3.5 years instead of 25 years, and I had money to spare for a desperately needed new car.

God does not want you to be poor, but he wants to be number one in your life, your best friend, so he can help you survive the coming shipwreck. He loves you and is waiting for you.

Thank you for reading.

Kevin Davis

SEPTEMBER 2018 POSTSCRIPT

Are we any closer to a crash this year as I predicted when I wrote the essay entitled We’re All On The Titanic back in February and March? David Brady, ex-foreign exchange trader and astute financial analyst thinks so and so do I. I have just listened to him give an interview and here are my summary notes of what he had to say:

Since the last global financial crisis ten years ago we have had almost continual quantitative easing (QE) across most central banks in the developed world. The totality of this QE exactly mirrors the rise in the US stock market over the same ten years as measured by the S&P index. QE is like an alcoholic punch-bowl at a party. The longer the party goes the more everyone loses touch with reality.

However, in the last year or so QE has reversed to become quantitative tightening (QT). The US Fed is draining their economies money supply by $50 billion a month as of this October. This amounts to $150 billion before Christmas 2018. The Europeans are also tapering their QE. The Japanese are engaged in a stealth QT. Global analysts for the banking industry have crunched the numbers and have come up with a global liquidity equation that has just gone into tightening or is about to early next year. In other worlds more money is draining from the global economy than is entering it through new loans. Stocks cannot rise in this environment. And since the markets look about six months ahead, they should begin to sniff a crash soon.

At the same time the rising dollar has put huge pressure on heavily indebted emerging markets such as Brazil, Turkey and South Africa. The crisis of 1998 started in emerging markets and came back to western banks and nearly sunk them. The emerging markets have about $7.5 trillion in debts denominated in US dollars. As the US dollar rises the ability for emerging markets to raise capital in their own currency, convert it to US$, and pay their debts gets harder. With the US dollar at 96-9 on its index, there has already been great pain in these markets as evidenced by what is happening in Turkey. But the Fed needs this high dollar to keep attracting funds to cover treasury issuance while they drain cash. For a foreign investor in the US treasury market, a falling dollar would wipe out any meagre interest they earned in the USA by the time the bond was converted back to their rising home currency.

At the same time the Fed likes to see a high stock market as capital gains taxes from this source are one of the largest sources of revenue for the US government. The stock market is about 1.5 times the size of the US economy by capitalisation. This is why the Fed always seems to come to its rescue with QE and bailouts for “too big to fail” Wall St banks.

At the same time as the Fed’s QT, the US government under Trump is raising some $100 billion a month to fund its deficit spending and stimulus packages. This money is not coming from overseas as there is little interest in lending to the current administration. The local market depth is insufficient for raising some $100 billion a month from within the USA. This means the Fed will have to step in soon and fund the deficit spending as it did under Obama. This won’t look good while the market is booming, but will be legitimised after a stock market crash. If it doesn’t step in then the demand for cash by the government will begin to force interest rates up above the 3% level for the 10 year bond, the bench mark for all risk free lending around the world. This would force emerging markets into a meltdown, as well as the world’s real estate markets. It would also blow a huge hole in the US government budget as it already drains $300 billion from tax receipts to pay the interest on its loans.

So, in summary, the Fed wants to do three things:

- Keep interest rates low or the US government budget will blow up and…bankruptcy

- Keep the dollar up to keep money flowing into the USA, to keep interest rates low or…bankruptcy

- Prop up the stock market to keep money flowing into the US government or….bankruptcy

Now, if the trade war causes a fall or crash in the stock market the Fed will have a great excuse to halt its QT and halt its interest rate rises. They will have an excuse to begin to print money (QE) to bail out the stock market and quieten the bond markets, that is, reduce interest rates. But it will be at the cost of the strong dollar. Trump wants a lower dollar as do exporters and US multinationals, so it is the one thing that can be sacrificed.

This explains why in the futures markets an entity called “the commercials”, the smart moneyed bankers, have just bet record numbers of futures contracts on a falling interest rate future. Not just record numbers of long contracts, but a new record by far. They are also near records in long futures contracts for the Japanese yen. Silver futures contracts have just gone net long for the first time ever, and the commercials futures contracts for the gold market went net long two weeks ago for the first time in this century.

Is there a high risk of a stock market crash in the next few months? Yes. The catalyst could be the trade war with China. The Fed has given two speeches in the last week where they have said they are ready for a crash! Why would they say this? The clue is in the looming 25% tariff hike on $200 billion worth of Chinese exports to the USA, due to kick in sometime on or soon after the 5th of September, in a week from now or less. The Chinese have already devalued their currency, the Yuan, by 10% in the last four months in preparation for large scale tariffs. If the new mega-round of tariffs comes into play it will send a shudder down the back of global trading systems. The last time the Chinese unilaterally devalued their currency in 2015 in response to a capital flight from their country, the S& P dropped over 10% in response. If they do something similar and larger this time it will crash the US stock market. They can’t retaliate with counter tariffs as the US doesn’t export that much to China, the trade balance is grossly one sided. Devaluing their currency is their best weapon.

The Chinese are also by far the largest buyers of gold in the world. Since China joined the IMF’s currency basket last year, the price of gold has started to mirror the movements in the Chinese Yuan almost perfectly. They do not want to pay any more for gold than what they were before. The other central banks have allowed them to do this as they all work together via the Bank of International Settlements, the central banker’s central bank. So, if there is a tariff wall put up by Trump, and China uses the only weapon it has left, the devaluation of its currency, then gold could go down even further than the crazy depressed prices we find it at today. These prices are artificial as evidenced by the huge number of short contracts that have been built up to keep it down.

A spike down in the price of gold would be short lived because a reversal to QE by the Fed, and a subsequent drop in the US dollar would be far bigger influences on future price movements than the Chinese intervening in the futures markets to suppress it. So we are very close to the big low in gold, possible a multi-generational low. A new round of QE would also be inflationary as the central banks try to pump the global economy back to health like they did after the GFC. This is also great for gold.

The bankers are lined up ready for the starting gun. The Fed is dropping hints. All we need now is to hear the bang, a stock market being shot by one of the two bullets of global QT or a tariff-inspired currency war. Oh, and we are coming up to October, always a great month for a crash, especially on a ten year anniversary.

I hope the above makes sense!